It is a given that insurers need to know the magnitude of their required capital as well as the drivers of solvency change. While many organizations get by with the minimum required insight into solvency, others are taking a more active approach to managing risk. Today, standards-based regulations such as Solvency II make calculating capital requirements more challenging, time-consuming, and computationally intensive. The modeling involved in creating a snapshot of solvency risks can be daunting, leading companies to look into those risks only when they are required or requested to do so. Given how quickly the economic environment can move today, this is a mistake. By the time organizations notice stressed conditions, it might require drastic adjustments or, even worse, be too late to rectify without adverse consequences. To remain competitive, insurers need tools that allow them to monitor solvency continuously.

The Phoenix Group is a consolidator of life insurance companies. It has a large number of with-profit and non-profit funds, each of which can be considered a company in its own right, i.e., there is a need to assess the solvency of each fund on a regular basis. Unlike many companies, the Phoenix Group had an internally developed system to monitor solvency. This approach erred on the side of simplicity and prudence when estimating movements in risk capital. The Phoenix Group engaged Milliman in a collaboration to develop an improved system that would increase accuracy and expand validity without sacrificing efficiency such that the company could better understand solvency, improve cash flow management, and monitor annual targets.

Working with The Phoenix Group, Milliman has developed an efficient and effective system for monitoring solvency on a daily basis, enabling management to see and respond to solvency-related risks in hours instead of in weeks or months. The solution combines advances in cloud computing, the power of Milliman’s MG-ALFA® financial modeling tool, and a well-designed analytical process to enable true daily solvency monitoring, resulting in significant risk management, agility, and competitive advantages. The system is designed to give managers easy access to actionable knowledge, supporting more active and engaged risk management practices. This unique solution also helps companies grow to better understand and manage solvency drivers over time. By observing which factors are most dynamic and which have the most impact on the bottom line, companies come to understand the elasticity and volatility of the risks they manage.

Why investing in daily solvency monitoring makes sense

There is no clear regulatory requirement necessitating daily solvency monitoring other than the exception: when a fund/entity is close to breaching regulatory requirements. Until now, the cost and complexity of anything other than a simplified estimation process would be beyond the reach of most insurers. Even with a highly cost-effective system, such as the one Milliman has developed for The Phoenix Group, the system provides a solution that is over and above what is required by the prudential regulations. And yet, it is an investment that makes a great deal of sense.

Companies without the ability to monitor their solvency position on demand implicitly assume the risk of markets shifting each day without proper reaction. Markets move with unprecedented speed, and the interconnections between market risks only grow stronger as global economies become more intertwined and mutually dependent. When combined with the ever-increasing complexity of asset and liability portfolios, it quickly becomes apparent that insurers cannot hope to use intuition or experience to respond to—or even stay aware of—the evolution of risks they must manage each day.

Insurers with daily solvency monitoring measures are empowered with the information they truly need to know and can make decisions based on that information. With a system in place, firms can more actively manage risk, reacting to variances in the marketplace before they become crises. Other benefits include observing the impact of stress and scenarios on the full balance sheet, allocating capital more efficiently relative to solvency thresholds, and adjusting investments more rapidly than others in the marketplace. All of these capabilities represent competitive advantages.

Additionally, a solution providing regular solvency monitoring makes regulatory compliance easier. Organizations are ready to produce reports when required or requested by regulators. This avoids the disruption and quality issues created by “fire drill” reporting. Through the use of estimated individual capital assessment (ICA) reports between valuation dates, it can also facilitate the production of ICA reports required in the UK by the Financial Services Authority (FSA). Organizations are also prepared to comply with the Use Test, which requires firms to demonstrate that solvency models are widely used in and play an important role in governance.

How the Milliman system works

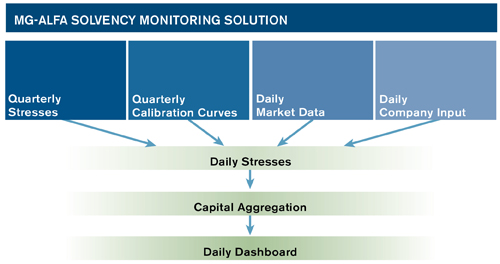

The implementation of daily solvency monitoring at The Phoenix Group uses stresses that are calculated quarterly to develop calibration curves for key variables. These curves are then fed updated, daily market and company data. When funneled through the curves, this data produces daily stresses, which are then correlated through the capital aggregation process and delivered to users in the form of a dashboard. The logic behind this design is to minimize the computing power and associated personnel resources necessary to produce the desired metrics while still delivering accurate results.

Quarterly calibration

As the name suggests, the daily solvency monitoring system runs on a daily basis. However, the amount of computational power it would take to recalculate stresses in full each day would be prohibitive. The system bypasses that problem by using regression curves that convert the stresses into polynomials. Daily market and company data serve as the coefficients of the polynomials, enabling the system to provide fast, consistent, actionable results.

The curves are recalculated each quarter to ensure that they remain up-to-date. Validation checks are also performed to ensure that the estimates produced by the curves adequately reconcile to the results of a full quarterly valuation run. With the quarterly stress curves in place, the system can perform its work thousands of times faster than a full valuation run.

Daily solvency process

For its daily runs, the solution draws on daily market data such as equity indices, the swap yield curve, exchange rates, interest rates, and so on, published by external sources. Data is validated, processed, and stored alongside of the latest version of company data, such as the real yield curve and shifts in asset volatility.

The model runs on a cloud-based compute engine that dynamically adjusts resources to ensure results will be delivered on time. Data values are plugged into the quarterly curves to update base and stress magnitudes, which in turn are used to process capital aggregation. Aggregated results are used to update the monitoring dashboard. Dashboard results requiring attention are flagged to make it a simple matter for managers to focus on and react to the most significant areas of risk. Results based on one day’s market data are available to managers when they arrive at work the next morning. It is a true daily monitoring system.

Benefits of daily solvency monitoring

The daily solvency monitoring system was designed to simplify the process of monitoring solvency risks. A key strategy is automation: once the quarterly calibration has been performed and the data sources are connected, the daily run is fully automated with no human intervention. Because of this automation, and because the system uses cloud computing resources rather than on-premises servers to do the computational heavy lifting, it enables organizations to allocate budget to analysis and action rather than processing. The ability to use massive computing resources for a short time at low cost means computing time is minimal. Reports are ready shortly after market data are available.

With reporting speed comes decision-making agility. Trends and variances are observed as they occur rather than waiting weeks or months for full reporting. The system is also designed for analytical flexibility. The impact of individual and aggregate risks can be measured at any point in time, and impacts can be assessed on an individual block or on the entire group. The system can output regulatory capital and company metrics including Solvency II Pillar 1 and Pillar 2 capital requirements, minimum capital requirements (MCR), risk margin, and more. As results build over time, it becomes clear which risks are most important to the company, as do the effectiveness of actions taken to control those risks.

For years, insurers have been encouraged by regulators (and market realities) to take a more active approach to managing risk, and daily solvency monitoring is an effective tool to this end. It provides actionable knowledge to managers based on the most up-to-date market data. To take full advantage of this capability, the dashboard can be customized to show key metrics with predefined thresholds for action, and the organization can develop action plans for threshold breaches. With this solution in place, insurers can manage risks in ways that keep much better pace with ever-accelerating global markets.

Charles Coatesworth is an actuary in Milliman's Philadelphia office.

Simon Frost is the Interim Head of Capital Management at Phoenix Life, part of the Phoenix Group.